This article comes courtesy of Shook Lin & Bok LLP. One of the leading and full-service commercial law firms in Singapore with a strong Asian presence and global reach. They have close to a century of rich legal heritage with a number of partners who are eminent lawyers in their respective areas of expertise. They have been recognised by reputable legal directories for their expertise in their major areas of practice including banking and finance, capital markets, corporate mergers and acquisitions, corporate real estate, employment, international arbitration, litigation and dispute resolution, regulatory, restructuring and insolvency, technology, media and telecommunications, and trust, asset and wealth management.

Client Update | Corporate Finance | June 2016

How an RTO Achieves a Win-Win for All

A reverse takeover, or “RTO” in short, is a transaction whereby a private company effectively gains a listing on the stock exchange by means of getting itself acquired by an existing listed company. This typically involves an existing listed company (“Listco”) (which can either be a Mainboard company or a Catalist company) acquiring the shares of a private company (“Target”) in consideration of issuance to the current owner of the Target (“Vendor”) a large number of new Listco shares, thus enabling the Vendor to take control of the Listco. Upon completion of the acquisition of the Target, the Listco will own the Target and the Target’s business will become part of the Listco’s group business. With new controlling shareholders in place at the Listco, there will typically be a change to the composition of the Listco’s board of directors. And in most recent cases, the new controlling shareholders would have the Listco dispose of its previous businesses such that post-RTO, the Listco’s sole business would be that of the Target’s. This effectively achieves the objective of the Target gaining a listing through the backdoor, also known as “backdoor listing”.

Reasons to pursue an RTO

An RTO can be an attractive route for a company to gain a listing for the following reasons:

(a) Agreed valuation and pricing upfront

In an RTO, the Listco and the Vendor would agree on the valuation of the Target, as well as the pricing of the consideration shares, at an early stage of the transaction. This would usually be at the point when the definitive sale and purchase agreement is signed. This allows for greater clarity and certainty with regard to the valuation and pricing of the Target at an early stage in the process.

(b) No requirement for underwriting and no need for book-building

In a typical RTO, the new shares being issued are the Listco consideration shares and these are issued only to the Vendor. There would therefore be no need for underwriting. Nor would there be a need for a book-building exercise to ensure sufficient investor interest in the issue. This would imply substantial savings in expenses otherwise associated with underwriting and book-building.

(c) Shareholder support

It is fairly common for the Listco to have an existing majority shareholder or a group of shareholders who collectively control a significant portion of the Listco shares and who would be on the Listco’s board of directors. These key shareholders would usually be supportive of the RTO and would provide the necessary majority shareholders’ approval at a general meeting of Listco shareholders where approval is sought for the RTO.

Recent RTOs in Singapore

One of the largest RTOs in recent memory is the reverse takeover of Ezyhealth Asia Pacific Ltd (“Ezyhealth”) by Wilmar Holdings Pte Ltd in 2006 (the “Wilmar RTO”). The Wilmar RTO transformed Ezyhealth (now known as Wilmar International Limited) from a small-scale healthcare provider into a multi-billion dollar agribusiness company. Other more recent RTOs in Singapore include:

(a) The reverse takeover of Hisaka Holdings Ltd. (“Hisaka”) by Regal International Holdings Pte. Ltd. (“Regal”) in 2014. Prior to the RTO, Hisaka was a precision manufacturer and upon its completion, the RTO resulted in Regal’s Malaysian property development business being injected into the group business of Hisaka. The listed entity is now known as Regal International Group Ltd and it operates two business divisions – the precision manufacturing business and the property development business.

(b) The reverse takeover of St James Holdings Limited (“St James”) by Perennial Real Estate Holdings Pte Ltd (“Perennial”) in 2014. Prior to the RTO, St James was in the entertainment business and owned a variety of bars and clubs. In this RTO, St James disposed of its entertainment business and Perennial’s property assets were injected into St James. The listed entity is now known as Perennial Real Estate Holdings Limited and is currently in the business of property development and management.

Further, in light of recent trends where companies are exploring privatisation or increasing their share prices to avoid being placed on the “minimum trading price” watchlist of the Singapore stock exchange (the “SGX-ST”), an RTO is a viable alternative option for such companies to retain their listing status on the SGX-ST. Such companies could utilise an RTO as an alternative to delisting by seeking to inject a fresh business into the Listco (which may be helpful to increase the value of the Listco), as well as to enable the existing businesses of the Listco to be privatised and divested.

Regulations and requirements for an RTO

An RTO requires interaction and compliance with the various different legislation and quasi-legislation that make up the regulatory framework here in Singapore, including the following:

(a) The listing rules of the SGX-ST (“SGX Listing Rules”)

The SGX Listing Rules govern the admission and listing of companies on the SGX-ST and prescribe the requirements applicable to an RTO. These pertain to matters such as the approvals required, admission criteria for the incoming Target’s business and the continuing obligations of the Listco (together with the Target, the “Enlarged Listco”) after the RTO. Different sets of SGX Listing Rules will be applicable depending on whether the Listco is listed on the Main Board or the Catalist of the SGX-ST.

(b) Securities and Futures Act (“SFA”)

Part XIII of the SFA and the Securities and Futures (Offers of Investments) (Shares and Debentures) Regulations (the “SFR”) provide for the regulation of the offering of shares in Singapore and prescribe detailed disclosure requirements in relation to an offering of shares (typically applied to an initial public offering (“IPO”)). As an RTO is in substance similar to an IPO, the RTO will have similar disclosure requirements as those which are applicable to an IPO under the SFA and the SFR.

(c) Singapore Code of Take-overs and Mergers (the “Take-over Code”)

Under the Take-over Code, amongst other rules, if the Vendor and its concert parties come to hold more than 30% of the shares in the Listco, the Vendor will need to make a mandatory general offer for all the remaining shares in the Listco. In an RTO, the Vendor will usually seek a waiver (“Whitewash Waiver”) from the Securities Industry Council of Singapore (“SIC”) from this obligation to make a mandatory general offer. The SIC may grant the Whitewash Waiver to the Vendor subject to the satisfaction of certain conditions (such as obtaining Listco shareholder approval for the whitewash). A Whitewash Waiver is one of the standard items typically obtained for the Vendor in the context of an RTO.

A brief description of the key items which would be addressed in an RTO, as required under the abovementioned regulatory framework, is set out below.

i. Admission Requirements

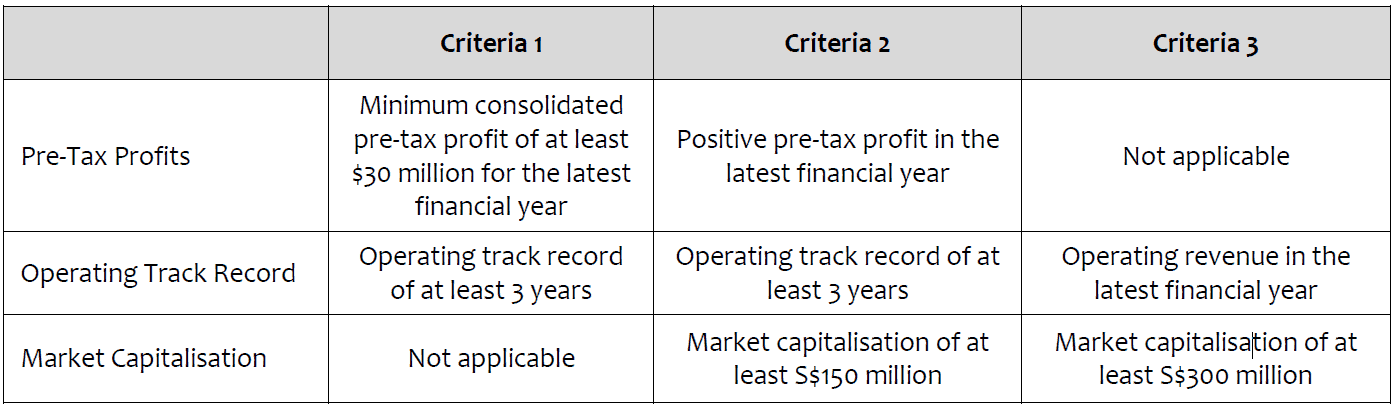

The Target and the Enlarged Listco need to fulfil certain listing admission requirements as set out in the SGX Listing Rules. For an RTO taking place on the Main Board, certain quantitative criteria relating to pre-tax profits, operating track record and market capitalisation will be applicable. A summary of the key quantitative criteria is set out below:

{kind=link}

The RTO will be able to proceed if the Target and Enlarged Listco (in relation to the market capitalisation component) are able to satisfy, amongst other requirements, any of the 3 sets of quantitative criteria set out in the table above.

For an RTO taking place on the Catalist, such minimum quantitative entry criteria are not expressly stipulated. The sponsor of the Enlarged Listco will apply its internal selection criteria to assess the suitability of the RTO and to decide whether the RTO may proceed.

ii. Announcement

After the terms of the RTO have been agreed between the Listco and the Vendor, the Listco will need to announce pertinent information relating to the RTO. Such information includes, amongst others, the particulars of the Target, a description of the Target’s business, the consideration for the acquisition, material conditions of the RTO and financial information of the Target.

iii. Seeking shareholder approval and issue of circular

An RTO is conditional upon the approval of shareholders of the Listco and the approval by the SGX-ST. With regard to shareholder approval, the Listco will need to prepare and issue a circular to its shareholders containing more detailed information relating to the Listco, the Target and the RTO. The circular will need to include additional information such as the history of the Target, a profile of its management and the proforma financial information of the Enlarged Listco.

iv. Valuation

The Listco will also need to appoint a competent and independent valuer to value the incoming business of the Target.

v. Minimum Share Issue Price

Since the consideration for the acquisition of the Target by the Listco is to be satisfied by the new issue of Listco shares to the Vendor, the price per share of the Listco, after adjusting for any share consolidation, must not be lower than (i) S$0.50 (in the case of a Main Board Listco); or (ii) S$0.20 (in the case of a Catalist Listco).

vi. Moratorium Undertakings

The Vendor will also need to provide contractual undertakings to observe a moratorium on the transfer or disposal of his Listco shares for a period of time after the completion of the RTO. The purpose of such a moratorium is to maintain his commitment to the Enlarged Listco and align his interests with that of public shareholders.

Our experience

The information above relates to a typical RTO scenario. Each RTO transaction is unique and will involve nuances that require different solutions. Having had extensive experience in advising on RTOs, we are able to provide our clients with practical legal solutions tailored specifically to their business’ particular requirements. Please feel free to contact us if you wish to know more about RTOs or explore other areas in which we may be of service to your business needs.

For more information, please contact:

Gwendolyn Gn

Partner

T: +65 6439 0708

E: gwendolyn.gn@shooklin.com

This information is provided for general information purposes only and does not constitute legal or other professional advice. It is not comprehensive. Specific advice should always be sought in relation to any legal issue. Shook Lin & Bok LLP does not accept any responsibility for any loss which may arise from reliance on the above information.

This article is written by Gwendolyn Gn from Shook Lin & Bok LLP.

This article does not constitute legal advice or a legal opinion on any matter discussed and, accordingly, it should not be relied upon. It should not be regarded as a comprehensive statement of the law and practice in this area. If you require any advice or information, please speak to practicing lawyer in your jurisdiction. No individual who is a member, partner, shareholder or consultant of, in or to any constituent part of Interstellar Group Pte. Ltd. accepts or assumes responsibility, or has any liability, to any person in respect of this article.