On 22 November 2018, the Thai Revenue Department (TRD) took another significant step towards tightening its transfer pricing compliance and enforcement regime with the release of “the Additional Revision of the Thai Revenue Code No.47 (TRC47)”.

Over the past five years, based on the Base Erosion and Profit Shifting (“BEPS”) initiatives of the OECD, many jurisdictions including the key trading partners of Thailand have introduced a series of measures to counteract transfer pricing abuse and other harmful tax practices. Although Thailand has been relatively slow to react, the passing of TRC47 is the clearest indication to date that the transfer pricing landscape in Thailand is about to undergo significant changes based on mandatory transfer pricing documentation and a strict penalty regime for non-compliance.

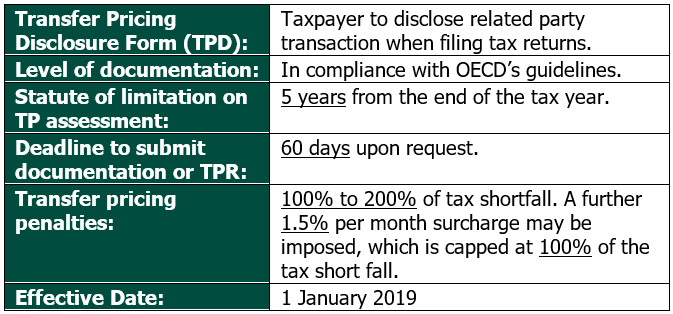

TRC47 provides the following five key points:

- The TRD is granted the authority to make adjustments to income and expenses for payments between related parties;

- Provides the definition of affiliated companies and the criteria thereunder;

- Establishes the reporting requirements for companies with income exceeding the threshold amount of THB 200 million (USD 6 million). These companies must submit a Transfer Pricing Disclosure Form (TPD) within 150 days from the company’s fiscal year-end;

- Directs that companies be prepared to provide the TRD with a formal transfer pricing report including documentation within 60 days of a formal request received from the TRD, which can be requested by TRD any time within five years from the submission of the TPD;

- Establishes penalties of up to THB 200,000 (appx. USD 6,000) for failure to comply with TRD’s documentation requirements. While the new TP law does not require contemporaneous documentation be in place prior to the taxpayer filing the tax return, subsequently prepared documentation may not provide adequate protection against penalties in the event that the TRD disagrees with the TP methodology adopted.

Overview of the New Transfer Pricing Regime of Thailand

Overview of the New Transfer Pricing Regime of Thailand

{kind=link}

With the effective date of 1 January 2019 only one month away it is recommended that taxpayers in Thailand take immediate steps to review their related party transactions to ensure adherence to transfer pricing principles and best practices. This will help to ensure efficiency in the preparation of transfer pricing documentation at the appropriate time.

Need legal advice?

If you are in need of legal advice, you can request a quote with DFDL lawyers or get a Quick consult with experienced lawyers. With Quick Consult, from a transparent, flat fee of $49, the lawyers will call you back on the phone within 1-2 days to answer your questions and give you legal advice.

This article is written by DFDL Lawyers.

This article was first published on the DFDL website.

This article does not constitute legal advice or a legal opinion on any matter discussed and, accordingly, it should not be relied upon. It should not be regarded as a comprehensive statement of the law and practice in this area. If you require any advice or information, please speak to practicing lawyer in your jurisdiction. No individual who is a member, partner, shareholder or consultant of, in or to any constituent part of Interstellar Group Pte. Ltd. accepts or assumes responsibility, or has any liability, to any person in respect of this article.