FinTech is on the rise globally

There has been a surge in popularity and interest in FinTech all over the world. Not only are startups spearheading FinTech innovation, but many banks and financial institutions are also exploring the idea of FinTech and committing significant resources to it.

FinTech also brings about new regulatory challenges

However, as I discussed in my last article on FinTech regulation, all potential FinTech innovators are aware of the need to apply for the relevant licences to operate in Singapore, and this can be difficult and time-consuming. FinTech companies I speak with have reservations coming under regulatory scrutiny and also about the high costs of compliance.

Regulations must keep up with the developments or risk stifling innovation

At the same time, from a regulatory perspective, the regulations in place might not be appropriate for new product or services as they were put in place to address concerns surrounding prior or existing products or services. Regulations are absolutely necessary and so regulators walk the fine line between safeguarding the integrity of the system and stifling great innovations that could bring our economies forward.

What is a Regulatory Sandbox?

A regulatory sandbox is a constructed well-defined space, within which companies can experiment with innovative FinTech solutions in a relaxed regulatory environment and with the support of a national regulator for a limited period of time while they validate and test their business model. It will allow innovators to experiment and develop FinTech solutions in a safe environment.

The MAS Regulatory Sandbox is Singapore’s solution to make it easier for innovators to experiment and for the government to regulate

The Regulatory Sandbox by MAS is the first step at regulating FinTech without stifling innovation and allowing for experimentation.

The MAS will relax specific regulatory requirements which an applicant might be otherwise subject to.The Sandbox provides appropriate safeguards to contain the consequences for customers as the effects of failure are limited to the specific trial group.

By managing the sandbox, the MAS will also be better able to understand and work out specific FinTech regulations for the future economy.

The concept of a Regulatory Sandbox is REALLY new — Singapore is the second jurisdiction in the world to propose a Regulatory Sandbox after the UK

The United Kingdom’s Financial Conduct Authority was the first to propose such a scheme in 2015. Singapore is the second country to do so. Public feedback on the MAS Sandbox ended on 8 July 2016. Following the MAS’s consultation, countries such as Australia, Hong Kong, Malaysia, Thailand have each come up with their own version of the regulatory sandbox.

The exact implementation timeline of the Sandbox has not been stated. However, from what we have seen with other jurisdictions in the region such as Malaysia, which Regulatory Sandbox Framework came into effect on 18 October 2016, and Thailand, which central bank is set to invite firms to participate in their regulatory sandbox early next year, it is likely that MAS will finalise the Sandbox Guidelines in the coming months.

The first batch of Regulatory Sandbox FinTech startups should be decided by mid-2017

With the speed at which regulatory authorities in the region are moving with their regulatory sandbox framework, I would expect MAS’ first batch of applicants for the Sandbox to be decided by mid-2017. In the meantime, interested firms may approach MAS to discuss how their innovative FinTech solutions can be launched in the regulatory sandbox.

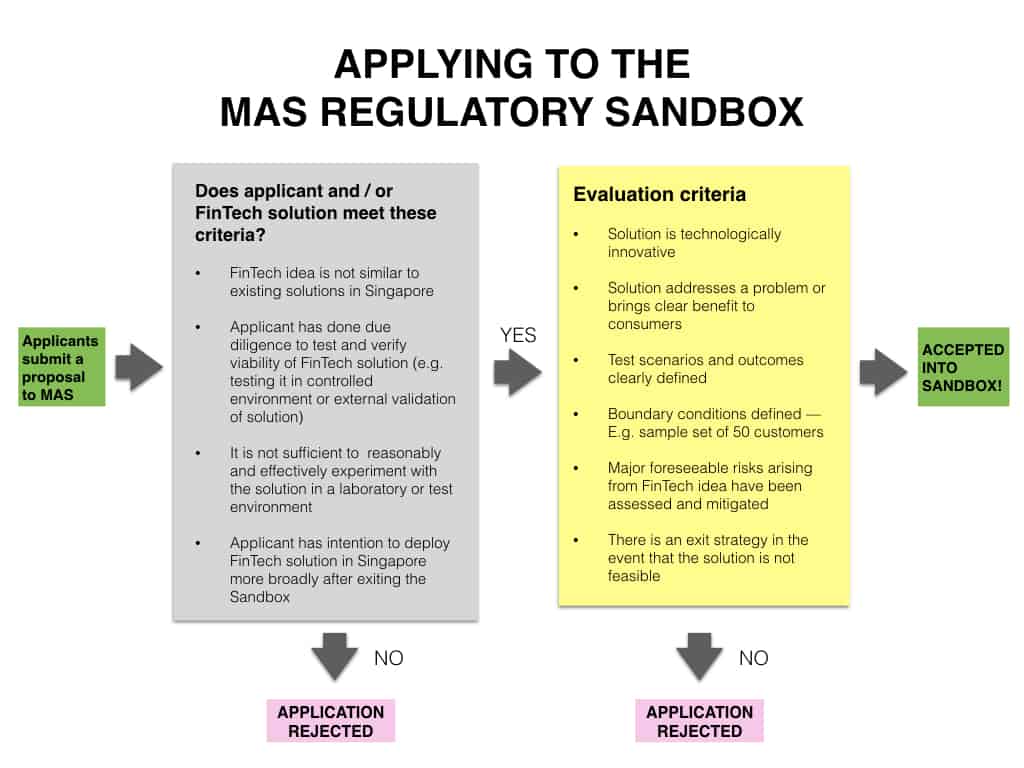

The proposed Sandbox can be broken down into 3 parts

The MAS has outlined some guidelines concerning the application and approval process of the sandbox. Here’s a snapshot of the main points regarding each part:

| Eligibility and application | Experimentation | Exiting |

|

|

|

PART 1 — Application; the first step to getting into the sandbox

Basic eligibility:

- Only NEW FinTech innovations are eligible (existing FinTech businesses operating are not)

- Open to both financial institutions and non-financial players

Interested innovators will have to submit a proposal and will have to clear 2 sets of criteria. The evaluation criteria will likely be the main filter used to investigate successful applications.

While the MAS has not released any details or examples of companies which will eventually qualify for the Sandbox, given the “FinTech Bridge” between United Kingdom and Singapore. The Regulatory Cooperation Agreement between the UK’s Financial Conduct Authority (FCA) and MAS enables the two regulators to refer fintech firms in their home countries to their counterparts across the globe.

{kind=link}

How strong are your chances to get approval to enter the MAS Regulatory Sandbox?

I believe that the first batch of companies in the sandbox will be assessed based on several indicators as adapted from the UK FCA’s requirements. FCA provides a helpful guide in the type of FinTech company/solution that will be successful in their Sandbox application.

How to use this checklist

Run through this checklist and the more checks you have, the stronger your application is. Some of these positive indicators are not binary but rather open to interpretation so it can be a good guide to how you need to position your FinTech idea. You might even use this list to tweak your business model to be more closely aligned with the criteria to improve your chances of acceptance to the Sandbox.

| Evaluation Criteria | Positive Indicators | ✓ | Comments |

| Is solution new / innovative?

|

The solution is technologically innovative

There are no other similar solutions existing in the market The solution does not look like artificial product differentiation |

The decision is entirely up to the regulator on whether the criteria to join the sandbox are met by the applicant.

A more diverse selection committee, which includes the private sector (eg, accelerators) would be ideal to grant a more neutral view on what kind of innovation is allowed in a Sandbox. |

|

| Does solution address a problem or brings benefits to consumers? | The innovation is likely to lead to a better deal for consumer directly or indirectly, eg through higher quality services or lower prices due to enhanced efficiency | ||

| Are test scenarios and outcomes clearly defined? | The business has no alternative means of engaging with the MAS or achieving the testing objective

The full authorisation process would be too costly/burdensome for the purposes of a short test of the viability of a particular innovation Examples of defined testing outcomes:

|

In contrast, the proposed Australia’s Sandbox requires that the Fintech business have an Australian Securities and Investments Commission (ASIC) approved “sandbox sponsor” which would be a not-for-profit industry association or other recognised entity, and would play a “gatekeeper” role by helping to ensure that the Fintech testing business has sound business model and is operated by fit and proper persons. | |

| Are test boundary conditions are defined? | Testing plans are well developed with clear objectives, parameters and success criteria.

Boundary conditions include:

|

MAS has not set out any guidelines for the boundary conditions.

Australia, however, have set specific guidelines (a) services cannot be provided to more than 100 retail clients; (b) each retail client with a maximum exposure limit of A$10,000; and (c) the total exposure of all clients (both retail and wholesale) is required to be less than A$5 million. |

|

| Any major foreseeable risks from the Fintech idea? Have they been assessed and mitigated? | Major foreseeable risks have been assessed and mitigated

The Fintech business has sufficient safeguards in place to protect consumers and is able to provide appropriate redress if required |

MAS has not set out what safeguards are necessary or sufficient to protect consumers.

Interestingly, in the UK, the Fintech business can only test their ideas on customers who have given informed consent to be included in such test. The FCA has said that it will agree on specific customer safeguards with businesses on a case-by-case basis. In Australia, the Fintech business must be a member of an ASIC-approved external dispute resolution scheme and have complied with the best interests duty and conflicted remuneration provisions as if it were licensed. The Fintech business must also clearly disclose that financial services are being provided in a testing environment. In both UK and Australia, the Fintech business must maintain adequate compensation arrangements for participating retail clients. |

|

| Is there a clear exit strategy? | Fintech business has an exit and transition plan for customers, in the event that the FinTech solution has to be discontinued, or can proceed to be deployed on a broader scale after exiting from the Sandbox | MAS would like that the Fintech solution be deployed in Singapore. However, this may be difficult to enforce. While the Fintech may have intention to deploy the product/solution in Singapore, Singapore may not be the right market after all, or the Fintech may find themselves having to change their strategy for survival or business reasons. |

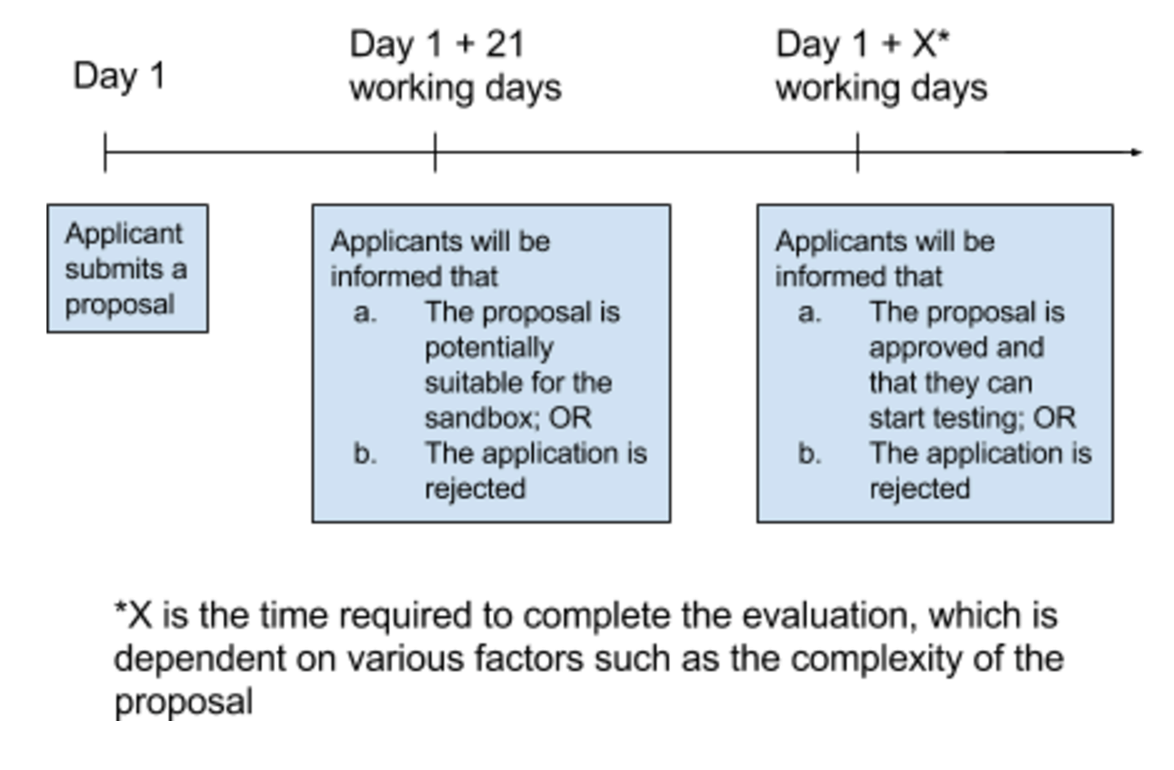

Applicants will be informed about their potential suitability within 21 working days while full approval of the application depends on the complexity of the project

{kind=link}

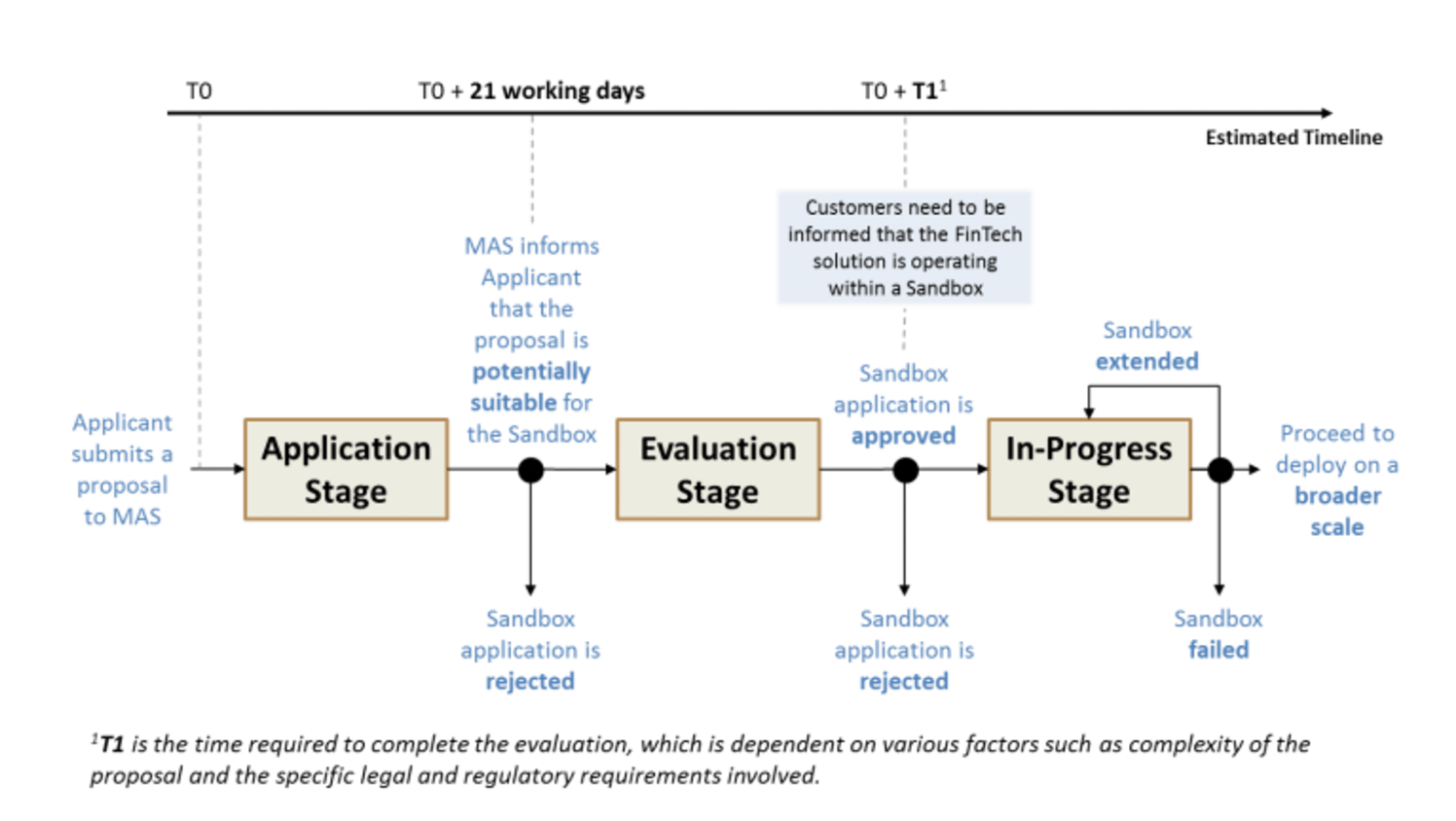

In evaluating the proposal, the MAS will consider the benefits brought about by the FinTech The applicant will be informed by the MAS on potential suitability for a Sandbox within 21 working days after receiving the completed application

The time required to assess the proposal is dependent on its complexity and the legal and regulatory requirements in question, and therefore unlike the application stage, no indicative timeline has been proposed for this stage of the application process. During this stage, the applicant may be allowed to make adjustments to its proposal after discussions with the MAS. The applicant would be informed in writing whether to proceed with the Sandbox. The MAS will review the submitted proposal and determine its potential suitability for a Sandbox.

The first batch of FinTech innovation in the Sandbox is likely to be varied

Judging from the first batch of FinTech innovations accepted by the UK’s FCA, it is likely that the companies chosen for Singapore’s sandbox will be similarly varied. The FCA accepted 24 applicants out of 69 applications (that’s a success rate of about 35%).

The applicants represented various sectors including: retail banking, insurance, advice and profiling and IPO.

PART II — Testing/Experimentation Period; subject to a time period that can be extended upon application

Period of experimentation is dependent on nature and complexity of FinTech Solution

Once approval has been granted by the MAS, the applicant then moves into the In-Progress stage whereby the specified Sandbox period commences. The period in which the applicant may operate within the Sandbox will be stipulated by the MAS. No specific timeline for the Sandbox testing period has been stipulated. This would depend on the nature and complexity of the FinTech solution proposed.

In contrast, Australia has a Sandbox testing period of 6 months, and 3 – 6 months in the United Kingdom. The Sandbox period in Malaysia is for a period of not more than 12 months, unless extended by the regulator but only where the FinTech solution has tested positively in general and it can be shown that the extended testing period is necessary to respond to specific issues or risks identified during the initial testing.

A longer period of testing certainly allows the FinTech business to undergo a more substantial phase of product development, and the regulator will concurrently be able to more accurately identify the regulatory issues arising.

If the above is any indication, it is likely that MAS will have a Sandbox testing period of not more than 12 months.

If an extension to the Sandbox period is required, the applicant is expected to apply to the MAS at least 1 month before the expiration date and provide reasons to support the application for extension.

Some Regulatory requirements might be relaxed during the testing period

During the testing period, certain regulatory requirements might be relaxed depending on the type of solution being tested, applicant and the proposal put forth. These requirements, which can be major obstacles to startups and emerging FinTech companies, include:

- Credit rating

- Minimum paid-up capital

- Track record

- Fund solvency and capital adequacy

- Licence fees

- Management experience

- Reputation

- Asset maintenance requirements etc

The examples listed above are not exhaustive, the precise relaxations would be determined by the MAS on a case-by-case basis in consultation with the Applicant.

How this greatly benefits FinTech startups.

This approach greatly benefits FinTech startups. Under the existing regime, a firm submits a licence application to MAS and indicates the specific exemptions (capital requirements, track record, fund solvency for example) it requires. The MAS may take a longer time to understand and clarify the risks before granting any exemptions, if at all. In the meantime, the FinTech firm faces an uncertain future, while it waits for MAS’s decision.

Under the Sandbox approach, a FinTech firm submits its application and states if it needs any regulatory requirements relaxed. It seems that if a FinTech firm cannot meet the “may be relaxed” regulatory requirements but meets the evaluation criteria and MAS is satisfied with its application proposal, MAS will approve the Sandbox application.

Some Regulatory requirements have to be maintained during the testing period

The MAS has stated that more fundamental obligations including confidentiality of client information;, fit and proper criteria on honesty and integrity; and prevention of money laundering (as discussed last week under Pillar 2 and Pillar 3) will not be relaxed.

The Sandbox can be terminated if the Applicant breaches any condition

If the Applicant breaching any condition imposed for the duration of the Sandbox, MAS has a right to terminate the Sandbox.

In the UK, the FCA is able to waive certain FCA rules and issue guidance, as well as (in rare cases where waiver or guidance is not possible) issue a “no enforcement” letter, giving a conditional undertaking that the FCA will not take disciplinary action against a sandbox institution.

ASIC in Australia is empowered to provide individual relief from the laws they administer and can, in some circumstances, issue no- action letters in relation to breaches of the law.

Whilst the MAS’ proposed powers do not currently include some of those granted to ASIC or the FCA, the MAS in it consultation paper, was seeking suggestions on additional forms of support that could be offered during the sandbox to encourage experimentation.

PART III — Exiting the Sandbox – The FinTech solution can either be scaled up or discontinued

{kind=link}

Source: MAS Consultation Paper on FinTech Regulatory Sandbox Guidelines

Once the Sandbox period expires after the designated experimentation period, the applicant will have to exit the Sandbox.

If Approved – Applicants can choose to scale up their FinTech solution

Upon exiting the sandbox, the MAS proposes that approved Applicants will be able to deploy their FinTech solution more broadly in Singapore, as long as:

- the sandbox has achieved its intended test outcomes; and

- the institution is able to fully comply with all relevant legal and regulatory obligations (meaning that any relaxation of regulatory obligations that applied in the sandbox would be lifted).

At this point, the applicant may choose to scale up its FinTech solution provided that the above requirements are met.

The important thing to keep in mind for Fintech start-ups is that, while the Sandbox provides a safe testing environment for start-ups which may not immediately be able to fulfil regulatory requirements (for example, minimum paid-up capital, fund solvency), the Fintech start-up in its product/solution testing period, would also need to plan early in the testing period on meeting these regulatory requirements, by speaking with investors for example. This is to prevent a situation where the Fintech start-up has to “cease operations” for a period of time after existing the Sandbox, until it can comply with the requisite MAS’ licensing obligations.

If Not Approved – the Fintech solution will be discontinued

When MAS or the Applicant is not satisfied that the Sandbox has achieved its intended test outcomes; the Applicant acknowledges that a critical flaw flaw cannot be reasonably resolved within the duration of the Sandbox; or MAS terminates the Sandbox due to reasons such as the Applicant breaching any condition imposed for the duration of the Sandbox – the Fintech solution will be discontinued.

The Applicant may, at its own discretion choose to discontinue their FinTech solution, and exit from the Sandbox.

Putting it all together

Financial services is without a doubt, one of the most highly regulated industries in the world.

In our current environment of highly disruptive new tech and immense innovation, with huge numbers of new entrants from outside the financial industry and banks rethinking traditional and existing business models, regulatory decisions will have even more impact.

The financial regulator has to be part of the innovation ecosystem, otherwise it can among other things greatly reduce the speed at which innovative ideas become workable products. In the FinTech environment, time to market is crucial.

As can be seen in the UK, Singapore, Hong Kong, Australia and other jurisdictions, regulators have been actively focused on financial services innovation, from fostering cross-border cooperation and setting up dedicated FinTech offices, to providing sandboxed environments for the safe testing of new tech. In addition to their sphere as policy makers and enforcers, these regulators are now also taking on a business development role.

In the sandboxed environment, the regulator is almost an “accelerator”. Accelerators programs usually have a set timeframe in which individual companies spend anywhere from a few weeks to a few months working with a group of mentors to build out their business and avoid problems along the way. Here, the regulator, FinTech business, consumers, incumbents are all involved, in collaboration. In this ecosystem, as new possibilities are discovered, the risks and limitations are uncovered quickly as well. The regulator, being part of the process, is thus also able to reflect these risks and policies into better and more relevant policies and laws, reducing regulatory uncertainty. This will naturally attract more business.

With this Sandbox, it allows FinTechs to experiment with their new and innovative solutions without the fear of punishment in the case of failure. It is not a free-for all however, and FinTechs would have to justify their admission to the regulatory Sandbox and subject themselves to MAS approval. It would be beneficial for all parties if the testing process could be clarified, so as to provide a more accessible direction for Sandbox participants in order to achieve a productive outcome.

This Sandbox is a right move in maintaining the reputation of Singapore as a leading financial centre and the need to create the space for disruptive experiments. As MAS reduces the regulatory uncertainty with respect to FinTech, Singapore as a financial centre will naturally become stronger.

Need help on your FinTech startup idea?

You might also want to read my earlier article with AsiaLawNetwork which is a simple, definitive guide to FinTech regulations in Singapore if you want to learn more.

If you need advice on any aspect of FinTech, you might consider having a Quick Consult with me where I can advise you and answer a specific question you may have on FinTech over a 15-minute discussion on the phone for a transparent, flat fee of S$69 here (or click here and click “Request for Quote” if you want to view other lawyers with similar experience in FinTech).

Alternatively, you could request a quotation from my firm ArrowGates LLC if you know exactly what you need.

One last note — I’ll be answering questions on FinTech at a Facebook Live Q&A with Sam Hall (Program Director at Startupbootcamp Fintech Singapore) so do join us HERE.

General Summary of MAS’ Regulatory Sandbox

| No. | Questions | Points | Comments |

| 1. | Who can play? | FinTech start up and financial institution (both new and existing), or any interested firm |

|

| 2. | What can be tested? | Any FinTech product or solution that is “technologically innovative” and not similar to those that are already being offered in Singapore |

|

| 3. | What are the limitations to playing in the Sandbox? | Not all sandbox applications will be approved |

|

| 4. | What are the conditions for playing in the Sandbox? | Not all Regulatory Sandboxes will be the same |

|

| Not all financial regulations can be relaxed. |

|

||

| 5. | How long can you play in the Sandbox? | The approval process and timeline are not fixed. |

|

| 6. | What happens after the Sandbox expires? | If approved by MAS – MAS proposes that approved Applicants will be able to deploy their FinTech solution more broadly in Singapore. |

(a) the sandbox has achieved its intended test outcomes; and (b) the institution is able to fully comply with all relevant legal and regulatory obligations (meaning that any relaxation of regulatory obligations that applied in the sandbox would be lifted). |

| If not approved by MAS – MAS can stop the deployment of the FinTech product |

|

This article is written by Yeong WanHsi from ArrowGates LLC and edited by Gabriel The from Asia Law Network.

This article does not constitute legal advice or a legal opinion on any matter discussed and, accordingly, it should not be relied upon. It should not be regarded as a comprehensive statement of the law and practice in this area. If you require any advice or information, please speak to practicing lawyer in your jurisdiction. No individual who is a member, partner, shareholder or consultant of, in or to any constituent part of Interstellar Group Pte. Ltd. accepts or assumes responsibility, or has any liability, to any person in respect of this article.