This is a three part series on Initial Coin Offerings (ICOs). In this series, lawyer Wanhsi Yeong will cover:

- An introduction to Initial Coin Offerings

- Overview of the current regulation of Initial Coin Offerings in various jurisdictions

- Framework of Initial Coin Offerings

In the first part of this series, WanHsi explains the characteristics, types, risks, benefits and examples of Initial Coin Offerings.

Introduction: What are ICOs?

In my previous article, I touched on the topic of cryptocurrencies. The pace at which cryptocurrencies are being adopted is astounding. For example, there are exchanges now trading in Bitcoin futures.

In that particular milieu of freshly launched coins is a newly famous transaction type we need to understand called the “Initial Coin Offering” or ICO.

An Initial Coin Offering, commonly referred to as an ICO, also called a “Token Sale/Initial token Offering”, is a fundraising mechanism in which new projects sell their underlying crypto tokens in exchange for more established coins such as Bitcoin and Ethereum. It’s somewhat similar to an Initial Public Offering (IPO) in which investors purchase shares of a company. These ICOs are often global offerings which can be created and/or accepted anonymously.

Perhaps the most famous ICO so far is that of Ethereum, which raised US$18 million in 2014 by selling tokens that facilitate online contracts. Today Ethereum-powered contracts are proliferating, and the tokens have a market cap of approximately US$ 60 billion as of mid-April 2018. Additionally, ICOData reports a total of 576 ICOs have been held in the first quarter of 2018 alone, raising approximately US$ 3.5 billion.

ICOs typically vary in nature and the respective organizations sell such digital coins/tokens for the purpose of obtaining public capital to fund software development, business operations, business development, community management or other initiatives.

As organizations continue to raise millions of dollars in ICOs, it is increasingly important for industry leaders and policymakers to understand the economic and regulatory landscape of ICOs. On the one hand, proponents believe that ICOs are a transformative approach to fundraising that enables consumers to benefit more directly from the popularity of new technologies. On the other hand, critics fret that ICOs occupy a regulatory grey area that could leave investors vulnerable to fraud and land startups in legal trouble. Given that ICOs are still in its infancy, both sides may be right.

Characteristics of ICOs?

Key Characteristics

Some key characteristics of an ICO include:

- Participation in a project, decentralized autonomous organization (DAO) or an economy.

- Coin ICOs generally sell participation in an economy, while token ICOs sell a right of ownership or royalties to a project or DAO.

- Owning tokens does not always give the investor the right to vote on the direction of a project or DAO, with the rights of the investor embedded within the structure of the ICO. Generally speaking, the investor will have input throughout a project lifespan.

- The majority of ICOs involve the creation of a defined number of coins or tokens prior to sale.

- ICO prices are usually established by the creators of the economy, project or DAO.

- ICOs may have multiple rounds of fund raising, with coins or tokens on offer, increasing in value until the release date. Early investors are likely to have greater rewards embedded within their tokens as an incentive.

- ICOs conclude once the coins or tokens are tradable in the open market.

So how then are ICOs different from traditional IPOs?

Here’s a table breaking down how ICOs are different from traditional IPOs:

| Initial Public Offerings (IPOs) | Initial Coin Offerings (ICOs) | |

|---|---|---|

| Ownership of Issuing Company | Investor obtains ownership based on the number of shares acquired | Investor usually does not obtain ownership, only obtain rights to a particular project |

| Decision making | Centralized, with the CEO and the board involved in the day-to-day operations of the business | Decentralized, giving the investor a material decision-making position |

| Financial data | Released in accordance with the rules of the exchange on which the IPO took place | Released by way of the blockchain or as outlined within the white paper and agreement with the investors |

| Taxes | Issuing company must pay taxes, with investors having to pay capital gains tax | Issuing company may not be subject to direct tax, only the investor being required to pay capital gains tax |

| Rounds of fundraising | One time sale with multiple intermediaries | Multiple rounds of fund raising, with few intermediaries (if any) |

| Regulation | Heavily regulated by the exchange on which the IPO took place | Regulation is comparatively laxed |

From the above table, it is evident that the key advantages of raising capital through ICOs include:

- The project, DAO or economy is not necessarily subject to direct taxation

- Sales of coins or tokens are direct, including multiple rounds, with few if any intermediaries required in the process.

Types of Tokens/Coins

There are generally 4 main types of tokens: Currency Tokens, Utility Tokens, Asset Tokens and Tokenised Securities. The table below helps to identify these four, and their attributes:

| Type of token/coin | Examples | Purpose |

|---|---|---|

| Currency Tokens/ Cryptocurrencies | Bitcoin (BTC), Bitcoin Cash (BCH), Litecoin (LTC), Ethereum (ETH), Monero (XMR), Stellar (XLM) | - Currency tokens represent a medium of value. - The currency value is purely based on speculation and user choice versus supply. - Cryptocurrencies differ from digital forms of fiat currencies as they are decentralized and thus function independently of a central bank. In addition, they do not require the use of a financial intermediary, and they use cryptography and a peer-to-peer network to ensure transaction security |

| Utility tokens | Ethereum (ETH), Ethereum Classic (ETC), Golem (GNT), Storj (STORJ), Filecoin (FIL), SiaCoin (SIA), Basic Attention Token (BAT) | Utility tokens are a medium for handling transactions. They may also provide users with access to a product or service. For example Filecoin provides users access to its decentralised cloud storage service. |

| Asset token | GoldMint (MNTP), LAToken (LA) | Asset tokens represent a particular physical asset, product or part thereof. For example, MNT tokenises Gold, LA tokenises a range of assets such as real estate and works of art. |

| Tokenised Securities / Equity tokens / Security Tokens | DAO, tZERO | Tokenised securities usually represent ownership of a debt or share of a company. For example tZERO (which is developing a token trading platform) is currently conducting a private offering of its security tokens. |

Benefits of ICOs

ICOs could prove to be a significant driver for financial access and inclusion by democratising access to investments. ICOs are popular for multiple reasons:

| For participants | For Founders |

|---|---|

| Investment potential: Cryptocurrencies that incorporate new technologies or are designed for unique purposes have the potential to become extremely valuable in the future. For example, 1 Ethereum token costs around 30 to 40 cents during its ICO. Its utility and exposure has caused its price to skyrocket. Moreover, more and more crypto-coins are beginning to come in the form of utility tokens. These tokens have specific functions and participants are able to purchase and use these tokens at a cheaper price. One example is Golem, which can be exchanged for high CPU processing power. | Global participant pool: Anyone can participate in ICOs, allowing for a global participant pool. Companies that require investments are able to reach out and pitch their ideas to interested parties worldwide by publishing a white paper. As such, it is easier to generate more capital due to a larger reach. Moreover, a large participant pool also leads to positive network effects. With each additional user, user experience improves as positive network effects are generated for such decentralised applications. This helps to sustain the operation, security and vitality of the network. If the users are equity token holders, they will more likely be invested in the growth and success of the network. |

| Access to projects worldwide: ICOs are readily available to anyone in the world so long as they have access to a computer and an internet connection. This makes ICOs a far more accessible investment option as opposed to trading on forex and stock exchanges which may be harder to access in some developing countries. Subject to jurisdictional requirements, anyone can contribute to an ICO, just like a Kickstarter or GoFundMe campaign. | Easy access to capital with low costs: With the hype surrounding ICOs, conducting an ICO can greatly increase a company’s exposure and attract a significant amount of investors which in turn provides easier access to capital. Furthermore, transaction costs associated with marketing and contribution settlement are significantly lower than traditional fundraising mechanisms. Tokens are marketed over the internet through the organisation’s website, whitepaper and other online platforms. |

| Easily transferable for liquidity: While most tokens that are newly introduced cannot be directly exchanged for liquidity on cryptocurrency exchanges, they are still relatively easy to liquidate these tokens. Using an exchange such as Binance or Shapeshifter that facilitates coin-to-coin exchanges, investors can exchange their tokens for more established cryptocurrencies such as Bitcoin and Ether. These coins have liquid markets on popular crypto-exchanges such as Gemini and CoinBase, and can be exchanged for traditional fiat currency. | No preconditions: Unlike traditional methods of raising funds, such as IPOs, the barriers to entry for conducting an ICO are much lower. There is no minimum paid-up capital required and little to no regulations or legal procedures that companies have to follow. Anyone with sufficient coding knowledge and a team of equally adept coders can conduct an ICO. Customized tokens can be generated through a number of platforms, including Ethereum, Stellar, Omni, NXT. |

| Transparent holdings and transaction records: With the usage of blockchain, all transaction records are made on a publicly accessible digital ledger, which increases transparency. However, this does not mean that the issuer is transparent with the software code and technology underlying the tokens. This has become a major cause for concern regarding ICOs. | Efficiency of blockchain technology: ICOs are conducted on platforms such as Ethereum which make use of distributed ledger technology. Through these platforms, users can write smart contracts that will issue tokens to the participant’s address. This requires much less effort and resources compared to the traditional fundraising process which includes sending out shareholder contracts etc. |

Risks of ICOs

Notwithstanding the benefits mentioned above, ICOs have generated their fair share of controversies. Broadly speaking, there are issues with consumer protection and market risks.

Consumer protection:

- Lack of due diligence: As ICOs are relatively new, there is no formal process to audit companies that conduct ICOs, hence there is a lack of accountability. Moreover, many organisations conduct token sales before even making significant progress coding the new crypto-coin. Companies usually only document their technology and business plans in a white paper, but this does not mean that the technology can be incorporated successfully or the organisation will be functional. Moreover, the security of funds is also questionable. Due to a lack of due diligence regulation, there may be bugs in the code. For example, the project DAO, which was the largest crowdfunded campaign then, collapsed after a hacker exploited a vulnerability in the DAO code and managed to siphon off a third of the total funding to a subsidiary account.

- Overinflated token valuation: As the sale of these tokens are not heavily regulated (and in certain cases, unregulated), the price of these tokens is purely based on market sentiment, demand and supply. Investors who do not fully comprehend the utility and value of the token may be contributing to ICOs based on speculation and the unfounded expectation that the prices of these tokens will likely increase. Essentially, investing becomes a gamble premised on the belief that a token might be the next Bitcoin or Ethereum and provide phenomenal resale profits. This belief is dangerous as it may perpetuate bubbles and even lead to Ponzi schemes and other scams as investors may be obtaining capital gains from newer investors blindly pouring in more capital.

- Risk of fraud: Potential frauds arising from illegitimate ICOs was one of China’s main justifications for a blanket ban on ICOs in 2017. In South Korea, 21 suspects were indicted for their involvement in a multi-million dollar, international pyramid scheme based on cryptocurrency mining, pocketing around US$250 million. ICOs are easy targets for scammers looking to make a quick profit due to the lack of regulations and relatively simple process of conducting an ICO. Organisations can simply create a bogus white paper that they have no intention of fulfilling and siphon off all the financial contributions from investors. In some cases, developers may also purposefully omit important details from their white paper to make their projects more attractive. The greatest consequence of all these scams is the declining public confidence in ICOs which may have implications on the viability of cryptocurrencies in the future.

- Security of transactions and tokens: During an ICO, the increased amount of transactions could place a huge strain on the blockchain causing a bottleneck, wherein miners are unable to record the transactions on the ledger fast enough. For example, during the Status ICO that raised $100 million, there was so much backlog in the network that many people saw their transactions fail. Security is also a significant concern as tokens may become compromised in certain scenarios. For example, tokens stored on crypto exchanges may be at risk of being stolen in the event that the exchange is hacked. In 2014, approximately 740,000 Bitcoins were stolen from the then popular Bitcoin exchange Mt. Gox. Customers lost all their assets that were kept on the exchange and the exchange entered into liquidation proceedings as a result of the hack. In addition, it is quite difficult to store some of the newer tokens in crypto-wallets. While tokens made on the Ethereum platform may be easily stored on Ether wallets, tokens made outside of the Ethereum platform can be very complicated to store in a secure location.

Market risks:

- Extreme price volatility: The prices of tokens are highly volatile. A quick glance at CoinMarketCap, a website which tracks the price changes of most cryptocurrencies, will reveal that the prices of these tokens are far from stable. Litecoin experienced close to a 300% gain in value in a matter of days in December 2017, and Bitcoin Cash surged from around US$1,200 to US$4,000 and fell to US$2,400 in just a span of a month, tokens certainly cannot be seen as stable investments. High-price volatility naturally leads to high risk for investors and could potentially be a reflection of underlying market manipulation.

- Market manipulation: The market for tokens could be manipulated in multiple ways such as pumping and dumping, spoofing, front-running and unscrupulous practices by “whales.” Whales refer to wealthy individuals who are able to manipulate ICOs by paying extremely high mining fees which helps them get first preference during ICOs. One example would be the BAT ICO. The BAT ICO was completed in 24 seconds and US$35 million was raised. It was reported that whales paid as much as US$2220 in transaction fees to ensure that they had first preference, which allowed them to subsequently sell these tokens at the premium. Due to a significant portion of the tokens being purchased by whales, not many people were able to participate in the BAT ICO.

- Government intervention: Cryptocurrencies are supposed to be decentralised and out of the governments’ control. However, recent controversy surrounding ICOs due to various scams and high-volatility in prices has resulted in several governments cracking down on ICOs. The U.S Securities and Exchange Commission (SEC) has already announced that ICOs should be regulated. Furthermore, increasing scrutiny on cryptocurrencies has led to countries such as China and South Korea to ban all ICOs since September 2017. With the fear that ICOs may be banned or heavily regulated, investors might be more wary when deciding whether to participate in these activities.

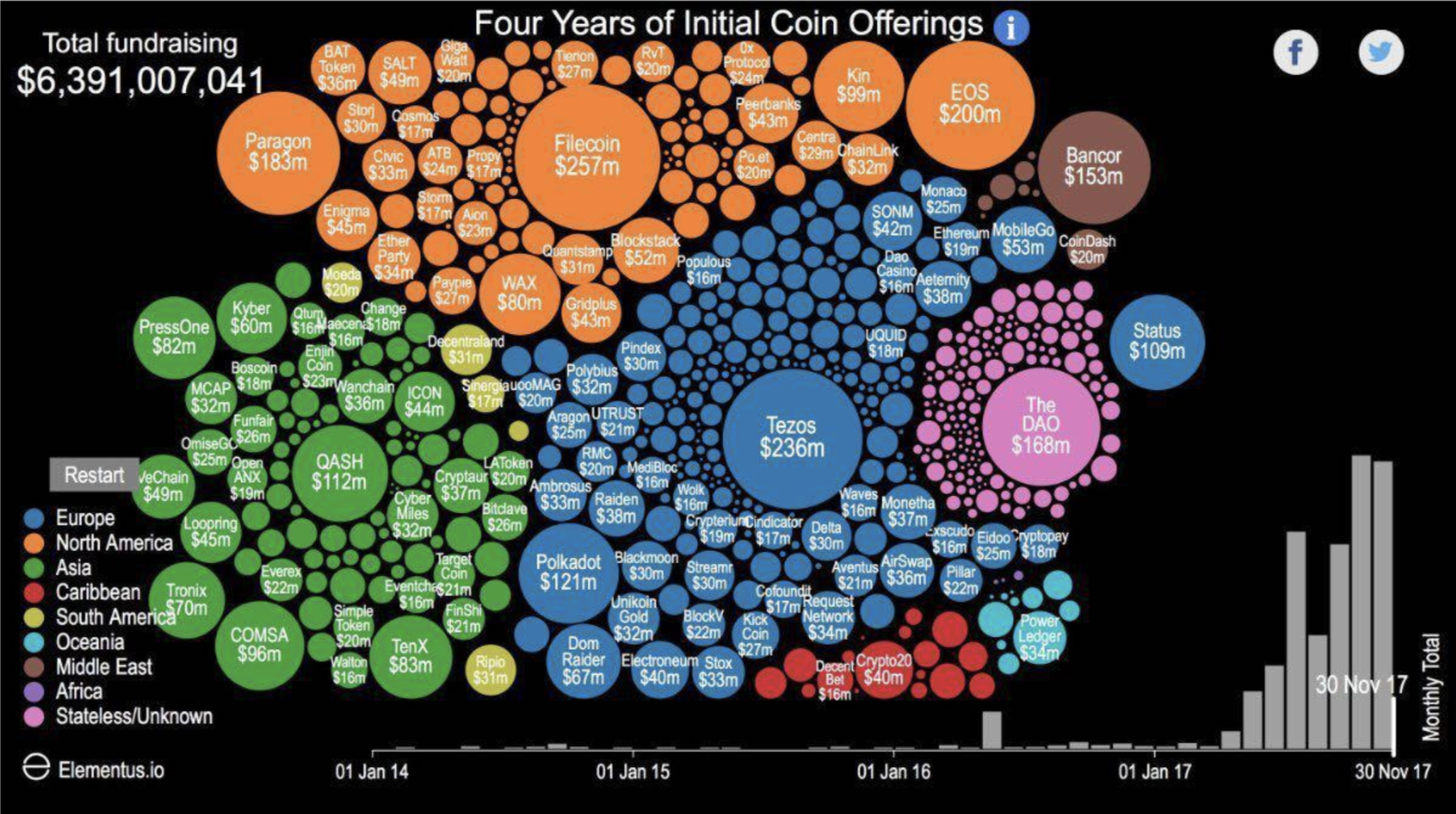

Examples of ICOs

The graph below depicts the number of ICOs conducted from 2014 to 2017. As can be observed, the number of ICOs spiked from the second quarter of 2017 with Europe, North America and Asia being the market leaders.

{kind=link}

Filecoin

Filecoin’s ICO was the most successful ICO of 2017. Concluded in September of 2017, it raised a record-breaking USD 257 million. This was impressive as unlike majority of ICOs, Filecoin only allowed accredited investors to partake in its token sale.

Filecoin aims to provide a decentralised storage network by making use of available storage space in data centres and hard drives around the world. Users can buy and sell unused storage on their personal computers on the Filecoin network. Filecoin’s tokens (also called Filecoin) can be used to buy additional storage space, or held as an investment. Users can earn Filecoin for hosting their files. Similar to the Bitcoin system, computers ‘compete’ to see which can store the most files. The computer which makes available the most storage space, and serves their data fastest on the network, will usually win the Filecoin.

TEZOS

The second biggest ICO of 2017 was the Tezos ICO. Unlike tokens built on the Ethereum platform, the Tezos project envisioned a cryptocurrency, called Tezzies, with its own ecosystem and decentralised blockchain. A key differentiator of Tezos is its self-amending cryptographic ledger nature which means that anyone invested into the network has voting power on future direction of the project (including features and funding). This allows its protocol to evolve and accommodate new innovations over time without the risk of hard forks splitting the markets (which happened to Ethereum and Bitcoin). While Tezos is not directly connected to Ethereum, it uses the concept of smart contracts, but makes it easier to apply formal verification which mathematically proves the correctness of the code governing a particular smart contract.

Although, the ICO concluded in July 2017, the Tezos project has yet to be launched as it has been riddled with legal issues. In December 2017, Reuters reported that the founders of Tezos, the Breitman couple, faced three class-action lawsuits in the United States, as “Plaintiffs allege federal securities law violations and that the fundraiser defrauded participants, who were told they were making non-refundable donations to the Swiss foundation. The lawsuits are seeking refunds and damages”. In addition, the couple were also embroiled in a legal dispute with Johann Gevers, the President of the Swiss-based TEZOS foundation that was supposed to help build the technology for TEZOS. The couple accused Gevers of enriching himself from the funds raised. In turn, the couple was accused of attempting to take-over the foundation and bypass the Swiss legal structure. This dispute was resolved in February 2018 with the stepping down of Gevers from this role in the foundation.

Recent ICOs in 2018

The ICO mania has most certainly carried onto 2018. In the first quarter alone, two prominent market giants from different fields jumped on the ICO bandwagon creating much buzz in the crypto world. These market giants are Telegram and Kodak.

Telegram

Perhaps one of the most talked about ICOs of 2018, Telegram, the messaging goliath, has raised approximately $1.7 billion from less than 200 private investors during two ICO presales. It plans to use the proceeds from the ICO to fund the development of its blockchain called Telegram Open Network (TON). TON is described to be an Ethereum-like ecosystem with service, apps and a store for digital goods.

According to the Wall Street Journal, Telegram has reportedly decided to cancel the public phase of its ICO. This may be not as surprising as Telegram was exempted from conventional securities registration requirement, given that the presale excluded retail investors. If it had decided to proceed with its public offering, it may have run into regulatory hurdles. Avoiding the spotlight especially when the SEC has been seeking to tighten the ICO space was probably a well calibrated decision by Telegram.

Kodak

In January, Kodak announced that it was going to launch its KODAKCoin ICO. KODAKCoin, the token that is to be issued, is designed to aide photographers have better control over the image rights of their portfolio. Photographers would be able to use the token to register their images on a distributed ledger and license them on Kodak’s upcoming platform, KodakOne.

Four months after the initial announcement, Kodak has finally revealed that the ICO will commence this month. The ICO is to be hosted on Cointopia and tokens are to be distributed under Simple Agreements for Future Tokens contracts. In its filing with the SEC, Kodak had indicated that it intends to raise up to USD$ 176.5 million. Given the success other famous companies have had with their ICOs, Kodak’s goal might be easily attained after all.

Closing observations

As can be seen from above, ICOs have quickly become popular with companies seeking funding due to the possibility of being able to raise significant amounts of money in a short period of time. Although the benefits of ICOs are indeed numerous, the risks associated with ICOs are very real and cannot be ignored.

Inadvertently, the spotlight on ICOs has also attracted the attention of regulators worldwide. In this regard, we shall examine in greater detail the position of authorities worldwide in relation to ICOs in Part 2 of this series. Do check in for my next article soon!

Need assistance with ICO matters?

If you need legal advice on Fintech matters, you can get a Quick Consult with Wanhsi or other lawyers. With Quick Consult, you can check out in minutes and for a transparent, flat fee, the lawyers will call you back on the phone within 1-2 days to answer your questions and give you legal advice.

{kind=link}

This article is written by Yeong WanHsi of Arrowgates LLC and edited by Seah Ern Xu of Asia Law Network.

You might be interested in these articles:

This article does not constitute legal advice or a legal opinion on any matter discussed and, accordingly, it should not be relied upon. It should not be regarded as a comprehensive statement of the law and practice in this area. If you require any advice or information, please speak to a practicing lawyer in your jurisdiction. No individual who is a member, partner, shareholder or consultant of, in or to any constituent part of Interstellar Group Pte. Ltd. accepts or assumes responsibility, or has any liability, to any person in respect of this article.